Efficient Frontier

William J. Bernstein

Efficient Frontier

William J. Bernstein

![]()

God Bless This Ponzi Scheme

For the past 30 years, the quintessential third-rail issue in American politics has been Social Security. And for most of that period, the Democrats have wielded it against the opposition with the same speed and devastation as a Mike Tyson right hook. But with the public’s increasing financial sophistication, the New Right has finally developed an effective counterpunch: Social Security is a lousy investment.

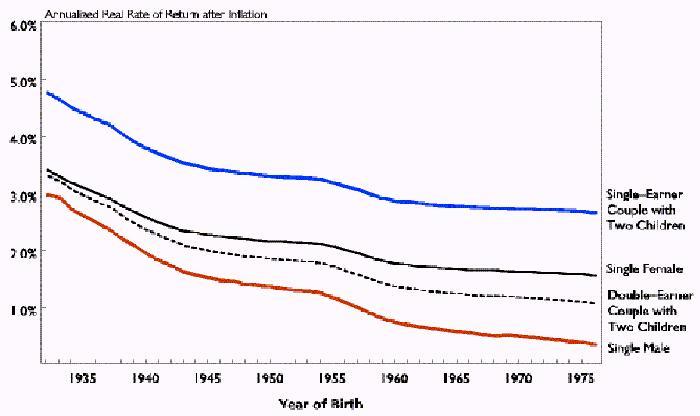

In the beginning, with the worker/retiree ratio in excess of 10, the average annualized real rate of return for the earliest participants was a robust 5%-6%. But with worsening demographics, returns fell. For future retirees, things will be even worse—real return rates steadily decline towards zero for most workers born after 1970. Moreover, certain family configurations are treated better than others. Married folks do better than singles. Men do worse than women because of their shortened life expectancy, and, for the same reason, black males do worst of all. Since benefits are not proportional to contributions, low-income participants do better than high-income ones; the real return for the latter group is now negative. A monograph from the American Heritage Institute plots the fall in real returns to later participants:

Writing in the Op-Ed section of the Wall Street Journal, former Fed governor Lawrence Lindsey pouted that he will not earn quite the return on Social Security as on his other retirement accounts:

Doing the math, I found that I would get all my money back three months short of my 83rd birthday. God willing, I will live well past this date, but the actuarial tables predict that I will fall about five years short. In other words, the expected real return on my Social Security contributions is negative. To add insult to injury, I will have paid taxes both on my contributions to the system and on 85% of the benefits I take out of the system. This makes the real after-tax return I can expect even more negative.

The problem with this sort of analysis is that not in anybody’s wildest imagination can Social Security be considered an investment operation. It is pass-through wealth redistribution, pure and simple. Today’s retirees are not paid from their past contributions; their checks instead come from currently-employed younger workers. The "Social Security Trust Fund" is merely a slip of paper denoting the part of the federal deficit owed by the Treasury to the Social Security Administration. It is no more an investment pool than the yellowing IOU from your cousin Bennie that resides in your desk drawer. The system is elegantly summed up by Jagadeesh Gokhale and Kevin Lansing of the Cleveland Fed:

Consider the following investment scenario. You turn over 10 percent of your salary each year to an investment manager who pools your contributions with those of others to form something that looks like a mutual fund. The manager assembles a portfolio that ends up earning a meager rate of return—less than 1 percent after adjusting for inflation.

Next, you learn that before you ever joined the fund, the manager made some unwise promises to the early investors. In particular, he guaranteed that they would receive very high rates of return—far exceeding the fund’s ability to pay, given its less-than-spectacular investment performance. Moreover, he handed out all sorts of cash bonuses along the way to keep the early investors happy. To maintain investor confidence, the manager used incoming cash from the new investors to make direct payments to the early investors.

This precarious setup actually worked for awhile. Now, however, like all pyramid schemes, the fund is on the brink of collapse because the supply of new investors has begun to dry up. Indeed, the manager informs you that you will have to increase your annual contribution to keep the fund solvent, and that you should reduce your expectations about future payoffs from this investment.

Personally, I find nothing inherently wrong with this. Long, long ago, around the turn of the last century, we lived in a world of unfettered Ayn-Randian capitalism, with minimal government interference in daily life and commerce. And no income tax¾ a gauzy sort of New-Right Valhalla. The only problem was that the reaction to this system's excesses and inequities led to a backlash that inflicted communism and fascism on most of the planet. The US escaped these modern plagues, but just barely. This was largely because our political leadership had the courage and foresight to modestly redistribute income and wealth via antitrust legislation, a progressive income tax, and finally, Social Security. Of course, social and political peace also require a functioning market economy—Bismark’s prototypical welfare system did not save German society from the depredations of the Versailles Treaty, and the social benefits of the communist state did not overcome its crippling economic and political disadvantages.

Social Security has not been a lousy investment; it never was an "investment" in the first place. It makes no sense to talk about the "rate of return" of a pass-through wealth redistribution scheme. But it also just may have saved the republic. (The ultimate irony of the interwar near-Götterdamerung of capitalism is that by severely depressing stock prices it set the stage for the spectacular returns now being drooled over by privatization enthusiasts.) When I become unhappy with the paltry reward I'm going to get from my FICA deductions, I think of my neighbor who lives down the road in a trailer park—call him Fred Smith. Fred's 75, has had a stroke, and worked all his life in a lumber mill, finding himself without a pension plan after a reorganization left him high and dry. Undoubtedly Fred has made a higher rate of return on his Social Security deductions than I'm going to make on mine. But unlike poor Mr. Lindsey, this doesn't bother me one bit. I'm as unhappy as everyone else with the huge crater made by the layers of deductions in my monthly paycheck. But the New Right just doesn't get it; that hole in our take-home is largely responsible for a prolonged period of social peace and prosperity nearly unique in world history.

The fact still remains that in two or three decades the system will be exhausted. The solution, say the critics, is simple: allow workers to opt out and invest in their own retirement accounts. After all, stocks have an annualized real return of 8%, right? Give Jim Glassman (Dow 36,000) a few minutes with a spreadsheet and he’ll show you how diverting just 2% of the FICA contribution into stocks will fund the plan. In short, in the words of the late John Raskob, "everybody ought to be rich." What's wrong with this picture? Plenty.

For starters, everybody cannot get rich investing in stocks at the same time. Consider the past 75 years in the capital markets. Yes, stocks have produced an 8% real return, but the real return of bonds has been only 2%. If you subsume the nation’s entire capital structure of stocks, bonds, real estate, and bank loans as a whole, its overall real return was probably closer to 5%-6%. The key point here is that a nation’s aggregate investment return is independent of its capital structure. In other words, if current stock valuations hold it is entirely possible that we may be sitting on the cusp of a new investment paradigm—one in which stock and bond returns are approximately equal. In addition, the flood of Social Security money into retirement and pension plans at the present demographic front end of the investment baby boom and the flood out at its back end in 20-30 years will further reduce the returns of both stocks and bonds. (For a fuller discussion of why everybody can't get rich with stocks at the same time, see The Heisenberg Equity Principle in the current issue of EF.)

Further, expecting the average worker to competently manage their own investments is akin to asking him or her to fly their own airliner. This is not an unfair analogy. Surveys show that a majority of people do not have a clear idea of the difference between stocks and bonds and have no grasp of their expected returns and risks. Even more importantly, there is no convincing evidence that the average investor has the knowledge and discipline to stay the course in tough times; as has happened so often in the past, they will most likely chase performance, buy high, and sell low. There are no high-quality data on the return of individual retirement accounts, but it is safe to assume that because of fund fees and frictional costs it will be at least 2% less than the aggregate national capital return—i.e., in the 3%-4% real range going forward.

A fast spreadsheet run shows that a worker earning a constant real salary from age 20 to 65 with a 10% savings rate requires a 4.03% real return to sustain a 20-year retirement at the same salary level. And even this is a wildly optimistic model, as most younger workers have relatively low incomes with zero savings. Start at age 30 and the required rate real of return is 5.74%, and if you delay retirement saving until age 40 you'll need an 8.86% real return. So, Houston, we have a problem¾ it is a mathematical certainty that privatizing even 5% of FICA deductions would prove woefully inadequate for most workers. At some point a government-sponsored privatized retirement plan would become The Mother of All Moral Hazards. Remember that there have been periods as long as 18 years with zero real stock returns. It is quite likely that this might occur between 2010 to 2030, as millions of boomers sell their securities. (And, as the old stockbroker’s joke goes, to whom?) It is hard to imagine the government not stepping in to rescue the armies of seniors with prematurely dry pension accounts.

Last, and not least, in a privatized system Fred Smith is not as likely to earn anywhere near the returns of the erstwhile Mr. Lindsey. While tolerable in a private retirement setting, a large disparity of returns in a government-sponsored system is politically and morally untenable.

Social Security privatization is not just fiscally risky, as suggested by Mr. Gore, but also socially and politically dangerous. Any national pension scheme must be executed in a uniform manner, if at all. Is such a system possible?

One tempting option would be to establish a government retirement fund. I imagine that Vanguard’s Gus Sauter could run the whole operation with a few dozen assistants for a fraction of a basis point. For starters, it would have to be established as a quasi-independent entity, a la the Fed, with its board serving long terms. Because of its prestige, it should have little problem attracting the cream of money managers, in spite of the modest salaries the agency would offer.

However, the possibilities for mischief at multiple levels are daunting. You don’t need a doctorate in political science to envision such an investment pool as the Mount Everest of pork; simply selecting the universe of eligible securities might prove to be a politically insurmountable task. And once you’re past that hurdle there would remain corporate governance issues to turn Fidel Castro's hair gray.

At the end of the day, it is wisest to conclude that in this arena the job of the federal government should be limited to maintaining social and political peace. It needs to be admitted, once and for all, that Social Security is simply a safety net, whose benefits will accrue most heavily to least fortunate. It is not now, and has never been, a retirement fund. (A modest suggestion. President Clinton should play to his strengths; appear on Oprah, tearfully confess that Social Security was in reality a vast Ponzi scheme, apologize for its sins, and beg the nation’s forgiveness.) Lastly, it should be accepted that the government should not be in the business of running or sanctioning retirement plans.

This is not to say that the government shouldn’t encourage private retirement saving as strongly as possible via legislation and education. It should dramatically expand pension portability and tax-deferred saving beyond the pitiful thicket of IRAs, 401(k)s, 403(b)s, and Keoghs we currently have. In an era when the 15th percentile of surviving spouse life expectancy is well north of age 90, it is monumentally stupid to mandate depletion of most retirement accounts by age 80.

But enmeshing Uncle Sam in the direct payroll funding of retirement is political and social napalm. Because of the coming demographic tidal wave, the safety net is badly frayed and unless reformed, it will break sometime in the next century. The FICA rate is already red-lined, so some combination of means testing and benefits reduction is inevitable. Let's do the job and move on.

![]()

![]()

![]()

![]()

Copyright © 2000, William J. Bernstein. All rights reserved.