Efficient Frontier

William J. Bernstein

Efficient Frontier

William J. Bernstein

![]()

Premium Investing

The complexities of the financial markets are such that economists often resort to models—analogies from simpler walks of life. And when considering equities, none is more useful than the insurance business.

When most folks think about insurance, it’s from the consumer’s perspective. The very act of living in our complex, technologically advanced, and highly litigious Western society exposes us to a number of financial risks, and we often find ourselves willing to pay someone else to take this risk off our hands. This payment is known as a premium.

Investment insight is gained by turning the tables around, and pretending that you’re an insurance company. Instead of paying others to handle your risk, others are paying you to bear theirs.

Assume for a moment for that you are "writing a put" on Microsoft for your friend Susan at a striking price of 80. In other words, you are providing her the privilege of selling the stock to you at $80 per share at her discretion, no matter what the actual market price. This is quite worthwhile to her if the price drops below 80, and can be thought of as insurance against at large drop in price of MSFT (as this is written, it's trading at 93). So if the price actually falls to 70, you are out $10 per share. For bearing this risk for her for the next 2 months, Susan pays you the market price of the put, which is $1.75 per share.

In this instance, you are operating in exactly the same manner as an insurance company—collecting a precise and well-defined (By the Black-Scholes equation. You don’t wanna know.) premium for bearing an equally well defined risk.

Most investment activities are not this well defined. With garden variety stock ownership, the premium is neither regular nor dependable. Instead you are insuring owners of large corporations against catastrophic loss of their capital by providing your own to them. The premium you collect is in the form of ownership; the price to the company is known as the "cost of capital." Again, we are simply turning the tables around. Instead of buying a stock for a price defined as dollars-per-share, we are providing insurance for shares-per-dollar. In the case of a sick company, such as Kmart, that price is very expensive in the sense that the company is obligated to give away a larger than normal percentage of its equity stake to raise a given amount of capital. And for a dot.com, capital is cheap; only a small portion of the company has to be given away to raise the same amount of capital. In financespeak, the huge risks associated with corporate ownership are thus syndicated among thousands of shareholders.

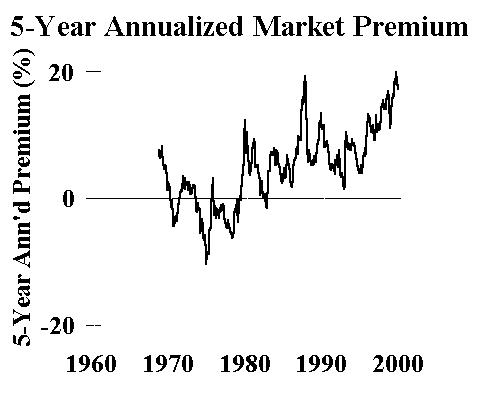

The most obvious difference with the insurance analogy is that the premium you actually realize is quite irregular, and may even be negative at times. How much premium are you collecting? It is simply the return of the risky security minus the return you’d have gotten by parking your money in a riskless investment (by convention, t bills). I’ve plotted the trailing 5-year annualized "market premium" for the past 36 years:

Source = Ken French/DFANotice that while it’s been persistently positive for the past few decades, things were a good deal rockier in the 60s and 70s. Over the entire period the premium was 5.65% annualized. It certainly wasn't a sure thing, being positive in 78% of the rolling 5-year periods.

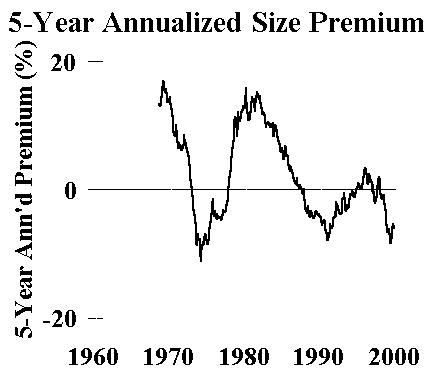

Is it possible to bear more risk, and thus earn still higher premiums? Yes. You can decide to invest in smaller companies, which are more likely to go poof than large ones. For the past 36 years the "small stock premium" (defined loosely as the return of the smallest half of companies on the NYSE minus the largest half) has been 1.71%. Its rolling 5-year return has been positive only 53% of the time:

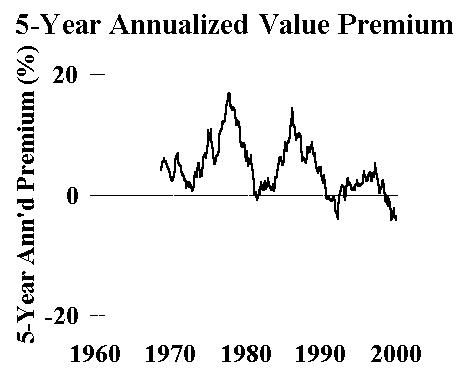

Source = Ken French/DFAThere is a third, and much more controversial, premium. According to efficient marketeers Eugene Fama and Kenneth French, if you are a real risk junkie and want to increase your premium payments even further, you can invest in value companies. These are the sickest puppies in the litter. Think Harvester, Kmart, Nissan. They are identified by their low valuations, such as price/book ratio. The 36-year premium for investing here (defined as the return of the stocks with the lowest P/B ratios minus the returns of the stocks with the highest P/Bs) has been 3.77% annualized. Surprisingly, this premium has been fairly consistent, being positive 87% of the time:

Source = Ken French/DFAIn fact, the reliability of the value premium has caused some to question whether this not really a free lunch, as opposed to a real "risk story." But that’s another column.

These 3 risk premiums—market, size, and value—have been researched extensively by Fama and French. They, and others, have shown all 3 to exist in the US market over a very long time period, as well as in many other countries. Are there other premia? Probably. There is likely a premium for investing in momentum stocks. The nature of the risk associated with momentum—if any—has yet to be determined.

The insurance analogy is also useful in other ways. For example, just as it would be unwise to provide fire insurance only to houses in the same block, or earthquake insurance only in San Francisco, so too is it unwise to invest only in one stock or industry. This kind of concentrated risk, easily avoided by diversifying your portfolio, is called "nonsystematic risk," and you are not rewarded for taking it. (Or, in the words of Paul Samuelson, you are not rewarded merely for going to Las Vegas.) Employees who own substantial amounts of their employer's stock expose themselves to industrial grade nonsystematic risk, for if their company suffers they may lose both their equity stake and their jobs at the same time.

Finally, the insurance analogy is useful when considering the dizzying array of options strategies employed by our largest institutions to "insure" their portfolios against a market meltdown. Think of a market crash as the financial equivalent of as a fire in which everybody has the same insurance company, and everybody’s house gets burned down. Such a situation is guaranteed to be highly disagreeable for both insurer and insured alike.

Ultimately, the rewards of the capital marketplace go to those who can most intelligently underwrite risk. A small example. Employees of cyclical, "value" companies should be particularly wary of value portfolios, as in the event of a severe recession both their job prospects and portfolios will suffer disproportionately. Letter carriers are in a better position to own value stocks.

If you do not diversify your risks appropriately, or if you cut and run at the first lash of risk's fiery tongue, then you should be very wary of equities.

![]()

![]()

![]()

![]()

Copyright © 2000, William J. Bernstein. All rights reserved.